What is an AARP Insurance Plan?

An AARP Medicare Insurance program is a supplement insurance plan that supplements original Medicare by providing additional benefits to the policy holder. The plans, labelled A thru N, come in various shapes and sizes, and will be appropriate to you depending on factors such as premium costs and the degree of coverage you are looking for.

What makes AARP insurance plans different from other supplement plans is not hard to figure out — they are endorsed by AARP. If you are not familiar with this crucial organization, now is your chance to get acquainted with them. Their mandate is to empower people over the age of 50, promoting individual agency and quality of life for the older sector of the American population.

When choosing supplemental medical insurance, wouldn’t you want to go with an option that is endorsed by an organization that has your best interests at heart? AARP Medical Insurance packages provide exactly that — comprehensive cover backed by a group that genuinely cares for your well being.

So what exactly do AARP Medigap Plans offer you? To understand this, it’s important to first explore what a supplement plan is, how it can be an indispensable part of your healthcare plan, and why the AARP name should influence your decision.

First, let’s have a look at Medicare Supplement plans and how they are structured.

What is a Medicare Supplement / Medigap?

Remember the words Shakespeare put into Juliet’s mouth, “A rose by any other name would smell as sweet?” Although slightly less poetic, he may very well have substituted “rose” with “Medicare Supplement Plans.”

Known as both Medicare Supplement Insurance or Medigap insurance, these plans are standardized by the government and offered by Medicare-approved providers.

If you are already familiar with Medicare, you will know that Medicare Part A deals with hospitalization and Medicare Part B with medical insurance. Supplement plans are intended to fill out your medical coverage where Medicare Parts A and B leave off. To be eligible for Medigap insurance, you have to be enrolled in Parts A and B.

Medicare covers approximately 80% of medical expenses in exchange for a deductible of $1,340 for Part A per coverage period and $183 for Part B per year in 2018. The aim of Medigap is to keep you covered for that remaining 20%. The benefits of supplementing your Original Medicare are multiple:

- Easy-to-budget medical expenses

- Choice of doctor and hospital provided they are Medicare approved. (This is a big one. Medicare Advantage plans — an alternative for comprehensive coverage — typically restrict you to a tight network of doctors and hospitals. Going outside of these bounds can lead to unforeseen out-of-pocket expenses. Not going outside of them can lead to having to go to hospitals and doctors that are inconveniently located, or simply not your providers of choice.)

- Ability to see a specialist without a referral from your family doctor

- Government-standardized plans, meaning you will not be taken for a ride by a private company.

- Lifetime coverage provided you keep up with your payments

- Your plan travels with you no matter where you go in the country, and in some cases, includes medical insurance for travel abroad.

When choosing a Medigap policy, many people are gravitating toward the AARP-approved plans — and with good reason. With a decision as important as your own health, wouldn’t you want to go with a choice endorsed by a body as respected as AARP?

We are going to take you on a journey through the history of AARP and let you into the values upon which they were founded on.

The History of AARP

Once upon a time, there was a forward-thinking retired high school principal named Dr. Ethel Percy Andrus. She saw the need to create an organization that would bind together retired teachers from all over the country based on her philosophy of productive aging. In this way of thinking, aging is not something to be feared. Seniors are important members of society with much to contribute. After all, aren’t they the ones with the life experience?

It was from this ideological basis that, in 1947, the National Retired Teachers Association (NRTA) was born.

Dr. Andrus was on a mission. She sought to bring healthcare to retired teachers who quite simply had none available to them at the time, either from government or private sources. Eventually, she found an insurance company willing to take on the task of insuring seniors.

Ten years later, and after numerous requests from people who had retired from other industries, Dr. Andrus realized the need for this service to extend beyond retired teachers. In 1958, she formed the American Association of Retired Persons, or AARP. Later, AARP blew onto the international stage, and ARPI (the Association of Retired Persons International) was formed.

Thanks to Dr. Andrus and her vision, AARP still serves millions of Americans today, with its numbers sitting at about 38 million members. It has offices across the country in 50 states. It remains committed to serving the aging population through an organization that is both nonprofit and nonpartisan.

The Core Principles of AARP

AARP’s mission is “to empower people to choose how they live as they age.”

While the structure of the organization has changed over the years, they still retain their initial commitment to promote independence and dignity for the elderly. They value the experience that older people bring into the world and believe it should be cherished.

Comprehensive medical coverage is a vital component of their mission, as their endorsement empowers people to make informed decisions about their coverage that will mean they are always in control of both their health and their finances.

Even if you decide not to join AARP, you can still enjoy the benefits of an AARP Medical Insurance package, as membership is not a requirement.

Let’s explore what joining the millions of AARP Medical Plan subscribers will do for you.

The Top 7 Benefits of AARP Medical Plans

- Trusted expertise

The reality is, AARP has been in the game of medical insurance for seniors since its inception. They know the ins and outs of the specific needs of their focus demographic. What’s more, at the heart of their motives is your well being. The organization was founded on principles that value the autonomy of the older sector of the population and appreciate what they have to offer.

- Peer Referrals

According to research conducted by AARP’s Medicare Supplement Plan division, 9 out of 10 plan holders were happy with their plans and willing to recommend them to family members. What a thumbs up!

- Diversity of Plans

As we will explore further in a moment, there is a range of AARP Medicare Supplement Insurance plans that suit a variety of needs. Whether you are looking for a plan with low monthly premiums and lower coverage, or are willing to pay high premiums for more comprehensive benefits, there is a plan that will match your needs set.

- Fewer Health Questions

When you first sign up for Medicare, you have six months to sign up for a supplement plan in what is called an open enrollment period. If you do not sign up for Medigap in this phase, you will more than likely be asked a range of health questions before an insurance company takes you on as a client. AARP Medicare Supplement plans are less subject to health questioning compared to other policies.

- No claim-forms to complete

If you have an aversion to bureaucracy, this may just be one of the biggest perks of a AARP Medicare supplement plan. Provided you stick to Medicare-approved healthcare providers, you will not have to spend your days filling out claim-forms that seem to go on for eternity in the hope that you will be compensated.

- Available across the country

AARP is represented in 50 states. If you want to find out more about the organization, or speak to a representative about Medicare options, you will not have to travel very far. Medicare supplement providers are also located across the nation, so you can easily find someone to deal with in person.

- Become Part of a Community of Shared Values

If you believe that seniors should be treated with respect and dignity, you will be among good company in the AARP community. This is not only about signing up for supplemental health coverage. It’s also about connecting to a network of people who believe in each other’s rights.

If you’re ready to dive into AARP Medigap insurance, we can almost bet what your next question is going to be — how much is this all going to cost?

AARP Insurance Rates

The best way to find out the exact rates for your specific situation is to contact SecureCare65 and one of our licensed agents. We offer a free quotation service that will consider all the factors that affect your life, from location, to medical conditions, to age, to how often you are looking to travel abroad.

Until you have that quote in hand, however, let’s take you through what each of the AARP supplement plans entails. That way, you can start to wrap your head around which option will be best for you.

What does an AARP Medicare Insurance Plan Cover?

Before we tell you what they do cover, it’s important to note that the following are NOT covered by any Medicare Supplement Plan:

- Prescription drugs

- Private nursing

- Vision

- Hearing

- Dental

- Long-term Care

If you are looking for coverage that includes these items, we would be happy to talk you through your various options.

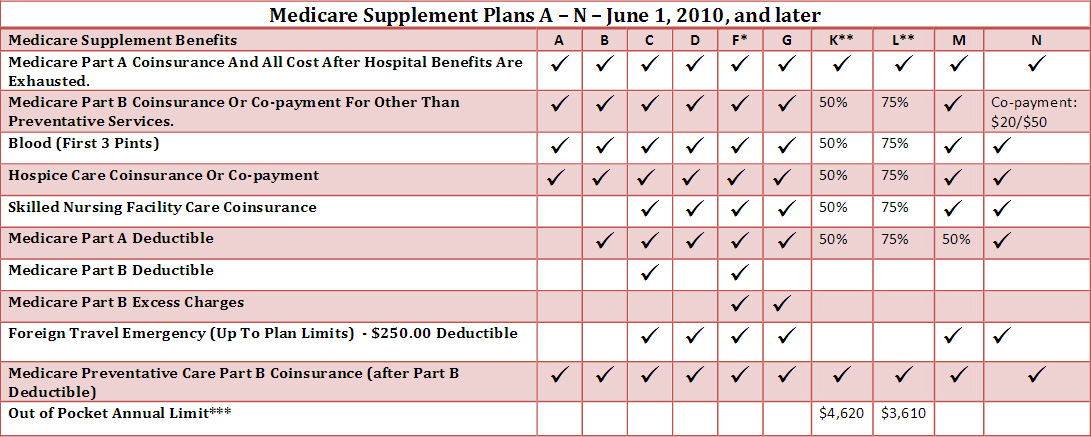

There are seven AARP Medicare Supplement Insurance Plans that offer varying degrees of coverage. As you will see, Plans K and L include an annual out-of-pocket spending limit, which the other plans do not.

|

Plan A |

Plan B |

Plan C |

Plan F |

Plan K |

Plan L |

Plan N |

Part A

(includes co-insurance + 365 hospital days after Medicare benefits end) |

100% |

100% |

100% |

100% |

100% |

100% |

100% |

Part B

(co-insurance / co-payment) |

100% |

100% |

100% |

100% |

50% |

75% |

Co-pay |

Blood

(first 3 pints each year) |

100% |

100% |

100% |

100% |

50% |

75% |

100% |

Hospice Care

(co-insurance / co-payment) |

100% |

100% |

100% |

100% |

50% |

75% |

100% |

Skilled Nursing Facility Care

(co-insurance / co-payment) |

|

|

100% |

100% |

50% |

75% |

100% |

Part A Deductible |

|

100% |

100% |

100% |

50% |

75% |

100% |

Part B Deductible |

|

|

100% |

100% |

|

|

|

Part B Excess Charges |

|

|

|

100% |

|

|

|

Foreign Travel

Emergency Care |

|

|

80% |

80% |

|

|

80% |

Annual Out-Of-Pocket

Spending Limit |

|

|

|

|

$4940 |

$2470 |

|

The various plans are loosely grouped in four categories based on how comprehensive the coverage is. Of course, the more widespread the coverage, the higher the premiums will be.

Let’s take a glance at what the most appropriate coverage might be for you based on your personal needs.

Plans A and B

If you are looking for lower monthly premiums, Plans A and B might be your best bet. Be warned, though — with lower premiums come lower benefits and the potential for higher out-of-pocket expenses. Even if you are fit and healthy now, you may want to consider coverage that accounts for the unknown future. It’s hard to imagine yourself in hospital if you have been healthy all your life, but the reality is it can happen to anyone. The last thing you want is to add financial stress to a health scare.

Plans C and F

Opting for Plans C and F means choosing near-full coverage. The trade-off is higher premiums for lower out-of-pocket costs. If you foresee that you will require hospitalization and other medical services, we would advise that it is worth paying the additional premium. This way, you can easily budget your medical expenses and stave off surprise costs.

Plans G

AARP Medicare supplement Plan G is almost the identical twin to AARP Medicare supplement Plan F except that it requires you to pay the Medicare Part B deductible of $183 (2018) annually. AARP Medicare Plan G is typically a much better value than Plan F as the premium savings over Plan F is usually much greater than the $183 Part B deductible which it requires you to pay.

Plans K and L

Like A and B, Plans K and L mean a lower monthly premium. Of course, with that comes less coverage of out-of-pocket costs, with many of the services being 50% or 75% covered for Plan K and L, respectively. Only consider these options if you are confident that you will not require a high degree of treatment in the future.

Plan N

Lastly, there’s Plan N. Plan N sits in the middle of the various options, offering mid-range premiums and mid-range benefits. The co-payment option for Plan B is worth noting, as it gives you the opportunity to pay lower premiums in exchange for co-payment on some office visits and on emergency visits that don’t result in admission.

Is an AARP Medicare Supplement a Good Choice for You?

The only way for us to answer this question for you is to have a conversation about your unique healthcare needs. You can either call us directly or fill in the form on our website for a free quotation.

Everyone’s needs are different. We want to ensure that yours are taken care of in a manner that takes into account the details of your situation. While Medicare Supplement plans are standardized, your unique requirements are not. That is why we would believe in talking directly to you so that together we can come up with a solution tailor-made to you.

Get in touch! We look forward to talking to you soon.